Market Recap (2/1/26)

Market Recap of the Week of Jan 25, 2026 - Feb 1, 2026

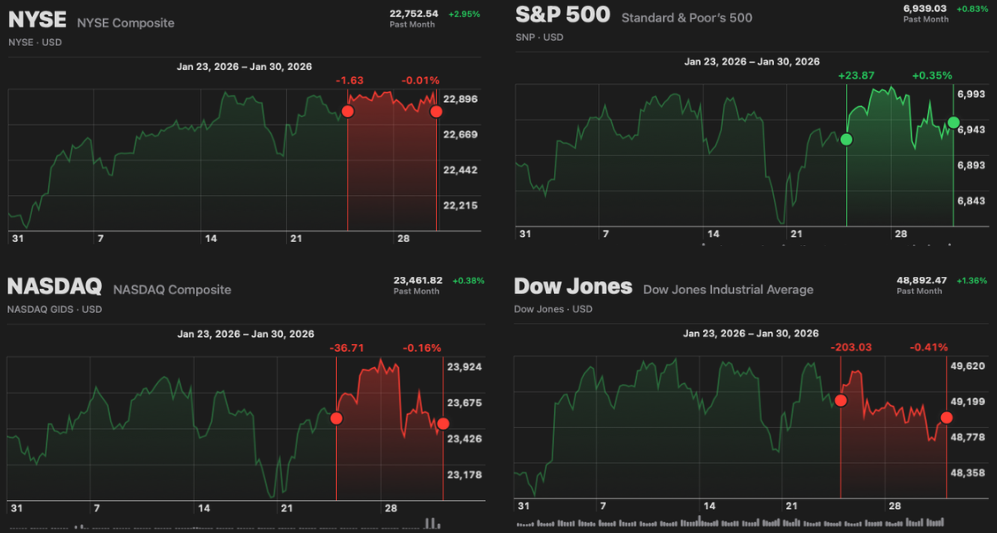

Source: Apple Stocks Application

Overall Market Trends:

The stock market ended the week little changed, with three of the four major indices finishing in the red. The New York Stock Exchange Composite (NYSE) fell 2 points (-0.01%), the NASDAQ Composite slipped 39 points (-0.16%), and the Dow Jones Industrial Average posted a weekly loss of 203 points (-0.41%). The S&P 500 was the sole winner, jumping 24 points (+0.35%).

Stocks rose on Monday as investors began to prepare for a slew of major earnings reports and the latest Federal Reserve interest rate decision. Over the weekend, President Trump had threatened to impose a 100% tariff on incoming goods to the U.S. from Canada if they made a trade deal with China. Current Canadian Prime Minister, Mark Carney, quickly responded, suggesting they have no intention of pursuing a potential free trade deal with China. The general consensus is that this threat will never come to fruition and is truly just a threat.

Big Tech continued to push the market higher throughout Tuesday’s trading session. Apple (NASDAQ: AAPL) rose just over 1% while Microsoft (NASDAQ: MSFT) advanced more than 2%. Health Insurance companies, however, saw major losses on Tuesday after the Centers for Medicare & Medicaid Services suggested increasing payments to Medicare Advantage issues in 2027. Humana (NYSE: HUM) and CVS Health (NYSE: CVS) plummeted 21% and 14%, respectively.

The market finished Wednesday dead even, with the S&P 500 reaching the 7,000 milestone for the first time. The earlier rise was boosted by chip stocks following Seagate Technology’s (NASDAQ: STX) 19% gain after beating estimates for earnings and revenue. The CEO also cited that demand for their artificial intelligence data storage was robust. However, markets pulled back later in the day after the Federal Reserve decided to keep rates steady and increase its economic growth assessment. Treasury yields increased following the decision, driven by remarks from the Fed suggesting that economic activity has become more stable and expanded at a “solid pace”. Some executives believe that the Fed will hold rates firm at the 3.5% to 3.75% until the end of Jerome Powell’s term in May due to heightened inflation paired with rising unemployment.

Thursday’s trading session saw sharp declines after a rough earnings report from Microsoft. The company slid nearly 10% as cloud growth had slowed and third-quarter operating margin guidance was soft. This caused software stocks to also take a tumble as investors have begun to fear that AI could potentially disrupt Microsoft’s business model. ServiceNow (NYSE: NOW), a cloud-based platform that automates workflows, collapsed 10% despite exceeding estimates on earnings and revenue. Salesforce (NYSE: CRM) and Oracle (NYSE: ORCL) also fell 6% and 2%, respectively, adding to the losses. On the other hand, Meta Platforms (NASDAQ: META) soared over 10% after releasing stronger-than-expected guidance for the company’s first-quarter sales. This gain was nowhere close to turning the tide for the day, resulting in losses across the market.

Stocks sank on Friday as technology companies remained in flux, despite the majority of investors approving of Trump’s nomination of Kevin Warsh for Federal Reserve chair. Warsh’s selection was heavily due to recent concerns regarding Fed independence. With his experience as a Fed governor and significant stance against inflation, much of the market sees him as being able to stand up to the president’s direction. As a result, the U.S. dollar jumped, suggesting investors approved of the pick. Spot gold and silver plummeted roughly 9% and 28%, respectively. Apple beat its earnings expectations and reported a surge in iPhone sales. Still, the company’s stock swung back and forth between gains and losses, ultimately ending the day up 0.47%. KLA Corp (NASDAQ: KLAC) tumbled 15% after its guidance showed a deceleration in growth. Verizon (NYSE: VZ), on the other hand, leaped roughly 12% after beating its earnings reports and giving a positive full-year earnings forecast.

Source: CNBC (Consumer News and Business Channel)

Past Earnings Report:

This Week in Crypto

Source: CoinMarketCap

Market Trends:

The crypto market pulled back sharply this week, finishing lower after a period of elevated volatility and heavy trading activity. Total crypto market capitalization fell over $300 billion (~10%), giving back a meaningful portion of recent gains as risk appetite cooled. Bitcoin (BTC) finished the week at $78,004 (-10.68%), while Ethereum (ETH) plummeted to $2,349 (-17.36%). Solana (SOL) also declined 14.55% to $103.57. Dogecoin (DOGE) saw heavier losses, falling 11.96% to $0.1054, and Cardano (ADA) ended the week down 14.32% at $0.2904. Hyperliquid (HYPE) was one of the few cryptocurrencies to see gains, surging 35.40% to $29.88. While the drawdown was significant, the market avoided a disorderly sell-off, instead moving through a controlled de-risking phase following a strong prior rally.

The crypto market started the week off strong, with prices pushing to new local highs. Total market cap briefly peaked above $3.0 trillion, supported by steady demand and continued optimism across the market from prior weeks, causing an increase in trading activity. Bitcoin held its price, despite investors rotating into more volatile altcoins.

That momentum, however, faded quickly as the week progressed. Selling pressure accelerated alongside a sharp increase in trading volume, signaling active repositioning rather than low-liquidity weakness. Derivatives markets drove much of the move as funding rates trended lower and leverage began to unwind. As prices rolled over, the pullback deepened, dragging total market cap toward the mid-$2.6 trillion range and erasing most of the early-week gains. Bitcoin dominance remained largely unchanged throughout the decline, indicating broad risk reduction rather than a defensive rotation into BTC.

By the end of the week, conditions had seemed to stabilize, though upside momentum remained limited. Bitcoin held above key psychological support, while Ethereum attempted to find a footing after significant underperformance. Trading volumes cooled from their mid-week highs, and derivatives funding turned slightly negative, suggesting traders were less aggressive with directional positioning. Open interest also declined modestly, pointing to partial deleveraging rather than a full washout.

Positioning and sentiment remained cautious into the close. Social and derivatives data reflected a market split between viewing the pullback as healthy consolidation and worrying it could extend further. With no clear macro or regulatory shock behind the move, price action appeared driven primarily by a post-rally reset in leverage and risk exposure. Bitcoin maintained its share of the market, Ethereum continued to lag slightly, and altcoins moved largely in line with the broader market as liquidity remained selective.

Live Crypto Markets:

Looking Towards the Future

Upcoming Important Economic Events:

Monday: S&P flash U.S. manufacturing PMI • ISM manufacturing

Tuesday: Job openings • S&P final U.S. services PMI • ISM services

Wednesday: ADP employment

Thursday: Initial jobless claims

Friday: U.S. employment report • U.S. unemployment rate • Consumer sentiment (prelim) • Consumer credit

Future Earnings Reports: