Market Recap (2/22/26)

Market Recap of the Week of Feb 15, 2026 - Feb 22, 2026

Source: Apple Stocks Application

Overall Market Trends:

The stock market rebounded over the course of last week’s shortened period after consecutive weeks of red. The New York Stock Exchange Composite (NYSE) rose 127 points (+0.54%), the NASDAQ Composite surged 336 points (+1.49%), the S&P 500 climbed 74 points (+1.09%), and the Dow Jones Industrial Average posted weekly gains of 127 points (+0.26%). These results were largely influenced by A.I. disruption fears and private credit concerns.

The market inched upwards on Tuesday despite persistent losses in the software industry. Investors continued to rotate out of software and into financial stocks. Some notable names were Citigroup (NYSE: CITI) and JPMorgan (NYSE: JPM), which rose 2.6% and 1.5%, respectively. On the other end of this rotation, Salesforce (NYSE: CRM) declined 3% while Oracle (NASDAQ: ORCL) tumbled nearly 4% on the day. The iShares Expanded Tech-Software Sector ETF (IGV), a key indicator of the software market, slipped over 2%. The software sector has been a major focus recently, with fears of artificial intelligence disruption continuing to grow. Many are concerned that the new technology could replace industry-specific software providers.

The rise propelled into Wednesday’s trading session as technology shares advanced, despite shaky minutes from the Federal Reserve’s most recent policy meeting. Meta Platforms (NASDAQ: META) announced on Tuesday that they plan to continue its data center buildout using millions of chips from the chip-giant, Nvidia (NASDAQ: NVDA), sending shares of Nvidia up over 1.5%. Amazon (NASDAQ: AMZN) also rose about 2% after regulatory filings showed that Pershing Square, Bill Ackman’s firm, increased its holdings in the company by 65% in Q4. Micron Technology (NASDAQ: MU) also climbed over 5% after Appaloosa Management grew its stake in the company. The market was not overly affected by the minutes from the Fed’s January meeting, which showed that, despite agreeing to hold rates steady, the Fed was split on the future direction of Monetary policy.

Stocks took a turn on Thursday amid geopolitical tension between the U.S. and Iran, combined with a move away from financials. The private credit sector collapsed after Blue Owl Capital (NYSE: OWL) reported that they plan on tightening investor liquidity after the company sold $.4 billion in loan assets. This sparked concerns about potential losses in the clouded private loans area, triggering Blackstone (NYSE: BX) and Apollo Global Management (NYSE: APO) to plummet over 5% each. Blue Owl also fell roughly 6%, capping a poor day for private credit companies. Software also continued to decline.

The market rebounded on Friday after a positive ruling from the Supreme Court. SCOTUS ruled against many of President Donald Trump’s tariffs through the International Emergency Economic Powers Act, citing that this law “does not authorize the President to impose tariffs.” Despite Trump responding by suggesting he would impose a new 10% global tariff, the market responded positively as they looked at this ruling as a way to ease the burden on companies affected by the tariffs, as well as the sticky inflation persisting in the U.S. economy. While this ruling was largely expected, many still question whether the U.S. will have to pay back the duties received from companies during the heightened tariff rates period.

Source: CNBC (Consumer News and Business Channel)

Past Earnings Report:

This Week in Crypto

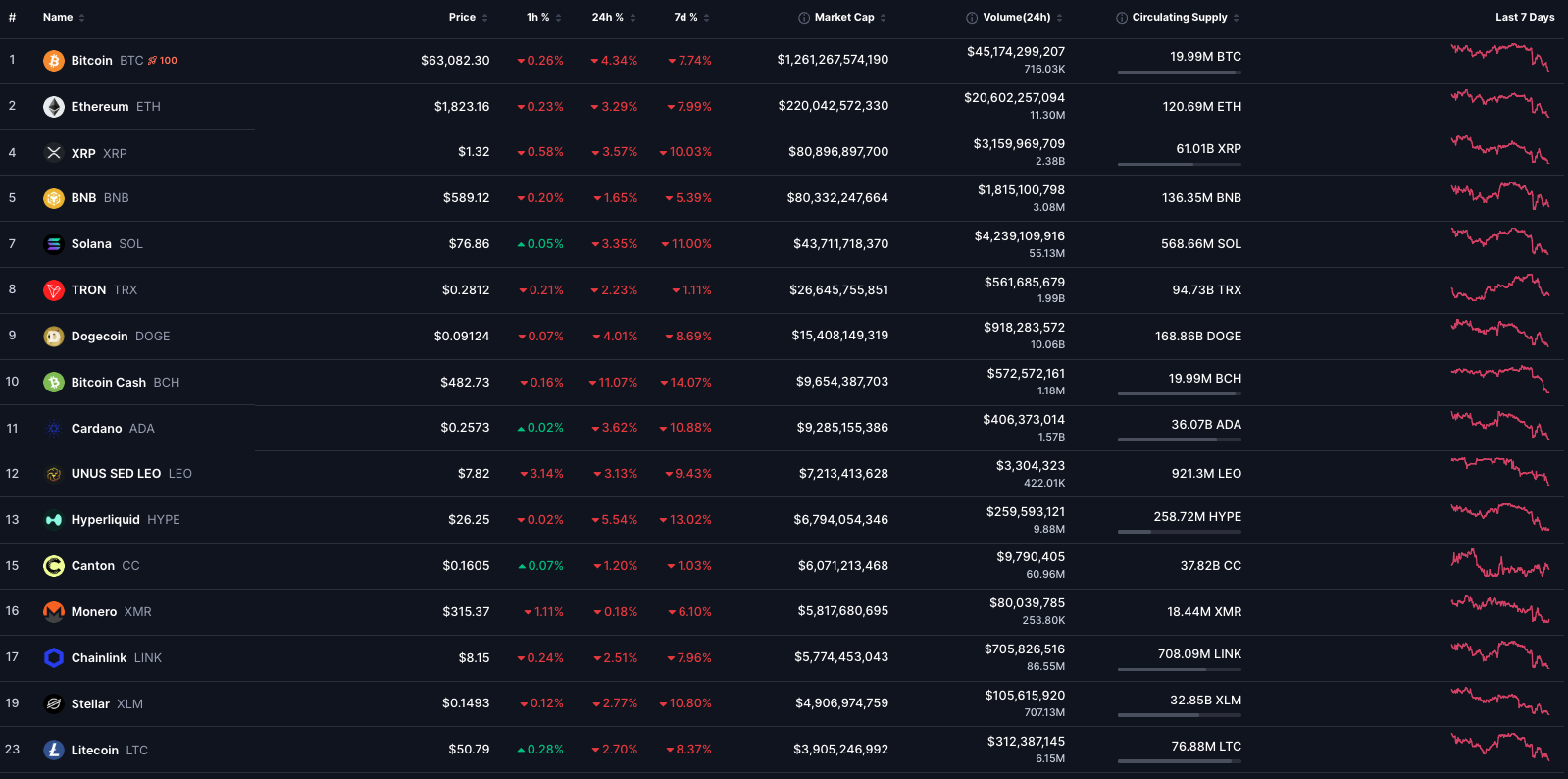

Source: CoinMarketCap

Market Trends:

The entirety of the crypto market continued to see sharp declines over the past week. Total market capitalization slipped from $2.42 trillion to roughly $2.33 trillion (-3.66%). Bitcoin (BTC) ended the week at $63,082 (-7.74%), while Ethereum (ETH) saw similar results, falling 7.99% to $1,823. Losses across large-cap altcoins varied but were all significant, with Binance Coin (BNB) down 5.39%, XRP falling 10.03%, and Solana (SOL) declining 11.00%. Dogecoin (DOGE) and Cardano (ADA) shed 8.69% and 10.88%, respectively. Bitcoin Cash (BCH) and Hyperliquid (HYPE) saw the harshest drops of the large-cap altcoins, finishing down 14.07% and 13.02%, respectively. These declines were largely due to decreased volume and shrinking derivatives exposure, while sentiment remained in the “extreme fear” category on the Fear & Greed Index.

Crypto prices moved slightly lower on Sunday, extending losses from the week before as the market continued to struggle to regain footing after the large sell-offs that occurred in January and now February. While total market capitalization remained elevated near the $2.4 trillion mark early in the session, participation began to thin and upside momentum remained weak. Bitcoin hovered in the mid-$60,000 range, but buying pressure was limited as traders remained defensive.

Monday marked the first meaningful acceleration in this week's fall. Total market cap dropped to a low $2.3 trillion range as selling pressure intensified across major coins in a relatively orderly fashion. While there were some liquidations present, none were extreme, suggesting that the weakness occurring was likely just sustained spot selling and cautious positioning rather than a leverage fallout.

Volatility started to slow on Tuesday, though prices remained stable throughout the day. Volume took a sharp hit, with 24h volume falling from 95.01 B on Monday to 79.24 B on Tuesday. The lack of dip-buying has made it clear that investors are not ready to aggressively re-risk, as sentiment remained in extreme fear territory.

A short relief bounce developed early on Wednesday but lacked follow-through. Bitcoin and Ethereum slightly recovered while open interest ticked higher due to short covering prior to the leveling. ETF activity continued to show net outflows, limiting confidence behind the move. The bounce appeared technical in nature rather than narrative-driven.

In common fashion, selling pressure returned on Thursday as the market moved toward local lows for the week. The total crypto market cap fell close to $2.30 trillion while several altcoins also extended their declines into double-digit weekly losses. Importantly, this downturn unfolded without a dramatic spike in forced liquidations. Instead, it reflected steady derisking and declining participation. Traders continued to reduce leverage ahead of the weekend, keeping volatility controlled but directional bias negative.

Friday offered the clearest attempt at stabilization. Trading volume increased notably, and prices across the board moved higher intraday. Bitcoin pushed off its lows and Ethereum followed, supported largely by short covering and tactical positioning rather than a major fundamental catalyst. Derivatives open interest briefly climbed, indicating some re-engagement from market participants. Risk assets more broadly also saw stabilization, which helped support crypto during the session.

By Saturday, momentum faded once again as markets entered the weekend. Prices consolidated near Friday’s levels, but open interest dropped sharply as traders aggressively trimmed leverage into thinner liquidity conditions. Volume fell considerably by late session, leaving the market in a quieter but still fragile state. Despite holding above the weekly lows, confidence remained limited.

Until spot demand meaningfully improves or institutional flows stabilize, rallies are likely to remain tactical and short-lived. For now, the market appears to be consolidating beneath resistance levels while participants wait for clearer direction.

Live Crypto Markets:

Looking Towards the Future

Upcoming Important Economic Events:

Monday: Fed governor Christopher Waller speaks

Tuesday: S&P Case-Shiller home price index (20 cities) • Various Fed Presidents and Governors speaking • Consumer confidence

Wednesday: Various Fed Presidents speaking

Thursday: Initial jobless claims • Fed Vice Chair for Supervision Michelle Bowman testifies to Congress

Friday: Delayed Producer Price Index report (PPI) • Core PPI • Construction Spending • Chicago Business Barometer (PMI)

Future Earnings Reports: